in the art world turn to New York")

")

")

Da cook

zscaler (Nasdaq:ZS) The stock has lagged its market-leading cybersecurity peers in recent months, which is somewhat difficult to understand given the company’s financial performance and valuation. This disintegration could be attributed to increased competition in SASE, or Zscaler’s or the company’s continued growth slowdown Continuous losses.

While Zscaler’s stock price may not be low enough to justify a buy based on valuation alone, the stock should reward investors willing to hold on to it through near-term volatility, unless Zscaler becomes an underachiever in its underlying market.

Market conditions

Zscaler reported that demand for Zero Trust security remains strong, although the macro environment remains challenging. Conditions appear to have stabilized, but customers are still scrutinizing deals. This is a sentiment widely reflected among other cybersecurity companies.

Despite the challenging market conditions, investors overall appear to be anticipating a significant re-acceleration of growth, with many cybersecurity stocks trading hot Near all-time highs. The optimism will likely come from the hype around AI, the ever-evolving threat landscape and SEC reporting requirements. Based on conversations with IT managers and CISOs, Zscaler expects zero trust budgets to increase in 2024. The company also refuted the idea of spend fatigue, suggesting that what customers are actually experiencing is ELA fatigue from paying for unused software.

Zscaler has not benefited from improved investor sentiment to the same extent as some cybersecurity companies. Competition can be a concern for investors, with an increasing number of companies offering a unified SASE solution to a single vendor. There was no indication that competition was an issue with Zscaler’s suspension or financial performance.

Zscaler offers a premium product but doesn’t seem concerned about pricing pressure. The company stated that cybersecurity is critical and customers are willing to pay for the best solutions. Zscaler also suggested that it could actually help customers save money by cutting back on things like hardware.

Investors may also have been spooked by the relatively weak results reported by Fortinet (FTNT) and Palo Alto Networks (PANW), along with Zscaler’s continued growth slowdown. Zscaler believes the role of firewalls is diminishing as demand for Zero Trust architectures grows, putting pressure on firewall vendors to create growth in other areas.

Zscaler still somewhat disparages legacy network security technologies, suggesting that threat actors continue to exploit vulnerabilities in firewalls and VPNs. Zscaler also believes that many companies are not truly offering Zero Trust architecture, but are just moving existing solutions to the cloud.

Zscaler business updates

Zero branch trust seems to be an area of focus for Zscaler at the moment. This is Zscaler’s Zero Trust SD-WAN, which the company believes could eventually eliminate firewalls in branch offices. Zscaler said it now has the first single-vendor SASE solution built on a Zero Trust architecture. Although I think there is an element of truth to this, basically every SASE vendor is trying to imply that they have the only true solution.

Zscaler has recently introduced several new products, although their impact on the business is likely to be minimal. Risk360 is a risk management platform that helps identify and address risks. Business Insights helps customers optimize spending on SaaS applications. Both Risk360 and Business Insights are growing rapidly, with demand for Risk360 driven by SEC disclosure requirements.

financial analysis

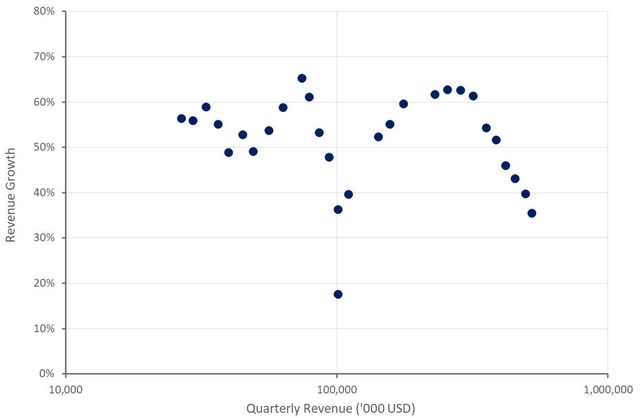

Zscaler’s revenue increased 35% year-over-year to $525 million in the second quarter, with billings increasing 27%. While this growth is objectively strong, especially given the demand environment and Zscaler’s scale, investors will likely focus more on slowing growth.

Third-quarter revenue is expected to be between $534 and $536 million, an increase of approximately 28% year over year at the midpoint. For the full year, Zscaler expects $2,118-$2,122 billion, representing growth of 31%. If growth stabilizes in the mid-to-high 20% range over the next 12 months, this should be supportive of Zscaler’s valuation.

Figure 1: Zscaler revenue growth (Source: Created by author using data from Zscaler)

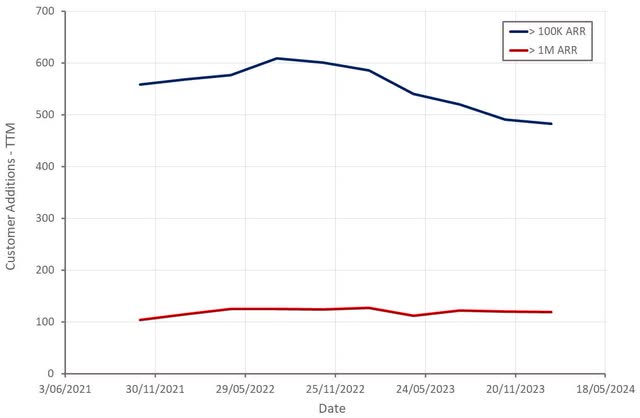

Zscaler added a record number of customers in the second quarter, but growth among larger customers was moderate. Zscaler now has a double-digit number of customers spending more than $10 million annually. $1 million plus ARR customers increased 31% year over year in Q2, and $100,000 plus ARR customers increased 21%.

Zscaler’s 12-month dollar retention rate was 117% in the second quarter. The company noted that some of the weakness here is due to the fact that it has had success driving more initial customer spending, which is clearly better from a financial perspective but results in less expansion later on.

Figure 2: Zscaler Net client additions (Source: Created by author using data from Zscaler)

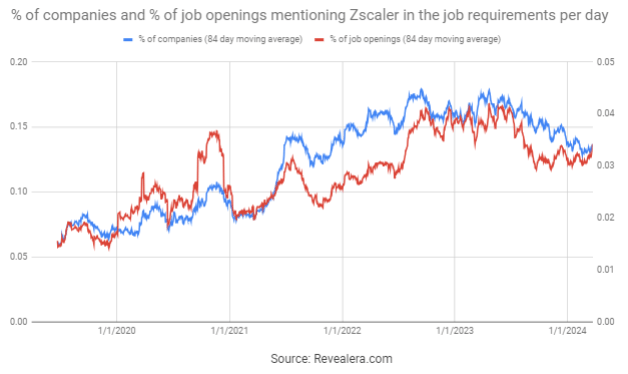

The number of job postings mentioning Zscaler in job requirements has declined over the past six to 12 months, which may be an indicator of a weak demand environment.

Figure 3: Job opportunities with Zscaler mentioned in the job requirements (Source: Revealera.com)

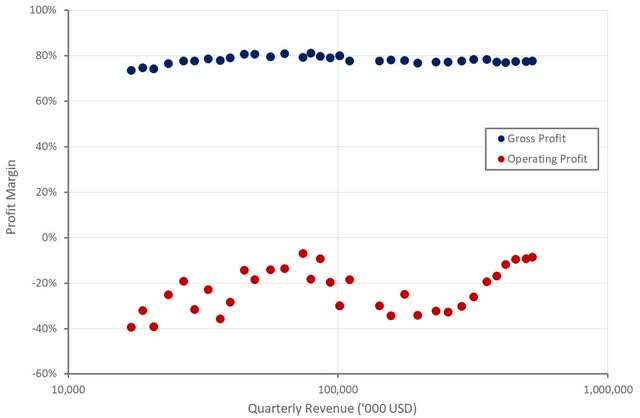

Zscaler’s gross margins have been fairly stable in recent quarters. Emerging products like ZDX and Zscaler for Workloads currently have lower margins and are therefore a drag at the moment. The increase in the depreciable life of its servers and networking equipment resulted in a 0.6% improvement in gross margins in the second quarter.

Zscaler’s operating profitability is also likely another area of concern for investors. Zscaler remains unprofitable on a GAAP basis and earnings have been weak in recent quarters.

Figure 4: Zscaler profit margins (Source: Created by author using data from Zscaler)

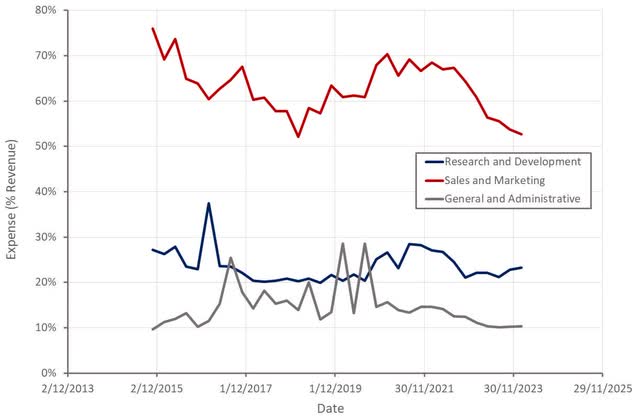

I don’t find this to be overly concerning though as Zscaler has high retention rates and a high average spend per customer. Investments in R&D currently lead to higher costs, which is not necessarily a bad thing.

Figure 5: Zscaler operating expenses (Source: Created by author using data from Zscaler)

Conclusion

Zscaler appears to be undervalued given its growth, profit margin, and strength of competitive position. Part of this may be because investors are concerned about increased competition in SASE. This may also reflect an irrational focus on the change in Zscaler’s growth at the absolute level of growth. Once Zscaler’s revenue growth rate stabilizes, the company could see its revenue expand double-digit to a level more reflective of the company’s prospects.

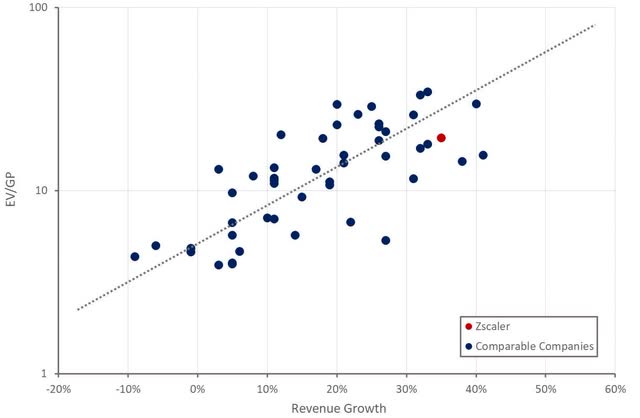

Figure 6: Zscaler relative rating (Source: Created by author using data from Seeking Alpha)

#Zscaler #Unpopular #Market #Leader #NASDAQZS

{kind=link}